The Cost of Doing Nothing

Consider an incorporated owner with $1M in corporate surplus, earning $500K in active business income. Here's what unexamined structure costs over time.

Idle Cash Earning Interest

$1M at 4% interest generates $40K/year taxed at ~50%.

Cost: ~$20K/year in tax on interest alone. Over 20 years, that's $400K+ in tax drag before compounding losses.

Investments in the Wrong Entity

$40K in passive income triggers SBD grind. Active business income loses its small business rate.

Cost: Up to $70K more corporate tax per year on business income when the SBD is fully eliminated.

No Estate Extraction Strategy

At death, CRA deems all shares sold at fair market value. Combined corporate and personal tax can exceed 50%.

Cost: On a $5M estate, $2M+ goes to CRA. Family may need to liquidate or borrow to pay the bill.

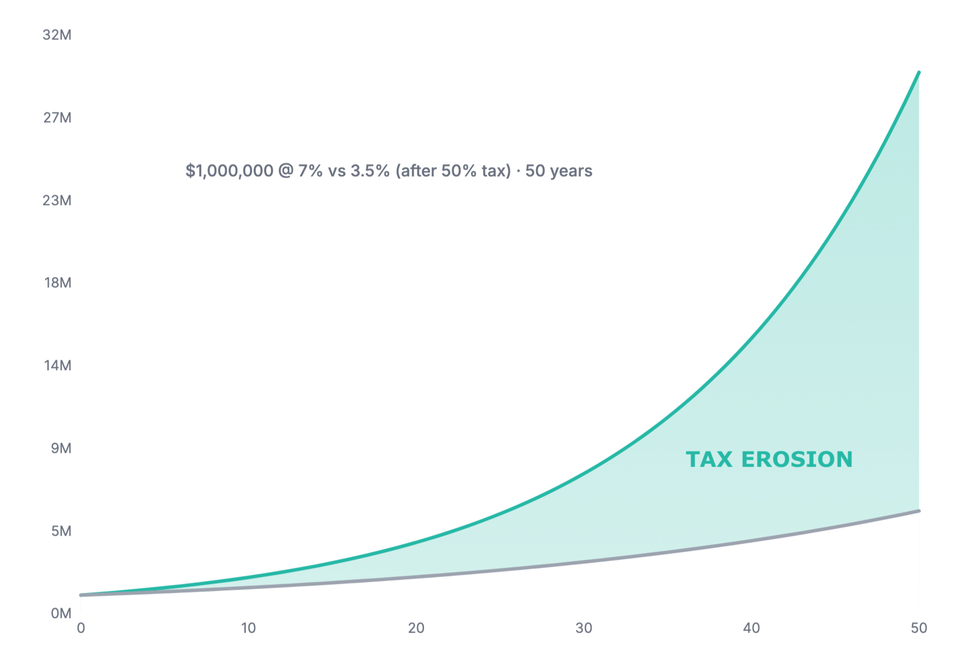

Tax-Inefficient Investment Structure

Funds generating interest and foreign dividends inside a corporation are taxed at ~50%. Capital gains: ~25%.

Cost: The wrong income type on $1M costs an extra $10-15K/year in tax. Over 20 years, that's $200-300K in lost compounding.

For this one owner, the combined cost of inaction could reach $2-4M over a lifetime.

This is an illustrative example for a single incorporated owner in Quebec. Assumptions: $1M corporate surplus, $500K active business income, 4% interest rate, Quebec combined rates, 20-year horizon. Actual results depend on your province, income level, investment structure, and personal circumstances.

Long-Term Wealth That Lasts

Put Every Dollar to Work

Corporate cash deployed in tax-efficient structures, not idle earning interest at punitive rates.

Build Lifetime Tax Reduction

Use HoldCo/OpCo separation, CDA, RDTOH, and corporate-class funds to reduce lifetime tax drag.

Create Estate Liquidity

Build insurance-backed liquidity for succession and estate needs, protecting what you've built.

Align with Family Legacy

Structure wealth to transfer efficiently to the next generation, not erode through tax inefficiency.

The real choice is erosion or compounding. We focus on what compounds.

Our 3-Step Approach to Generational Outcomes

Optimize for tax

Design around efficient income types and deferral to reduce drag and boost compounding.

Invest with leaders

Independent research to identify managers with durable edge and process discipline.

Structure to last

Align accounts, entities, and insurance to support succession and multi-gen continuity.

Our Investment Discipline

Built for Decades

We build portfolios designed for the long run, focusing on multi-generational wealth transfer, not short-term market noise.

Tax-Efficiency is Paramount

We prioritize after-tax returns. CDA, RDTOH, corporate-class funds: we use every tool to maximize what you keep.

Independent & Unbiased

We compare across providers and recommend what best fits your structure and objectives.

Who This Is For

This works best if you think in decades, value structure over quick wins, and already work with a solid CPA and lawyer. You want a partner who coordinates with your team, not someone who replaces it.

If you want fast answers, someone to make every decision for you, or guarantees, we're probably not the right fit. That's okay. Better to know early.

Services for Incorporated Owners

Corporate Cash & Investments

Keep reserves liquid yet working; design growth portfolios optimized for corporate tax.

Learn about corporate accounts →Life Insurance for Business Owners

Protect key people, fund buy–sell, build tax-sheltered value, plan estate liquidity.

Explore our insurance process →Personal Insurance & Investments

Align personal investments (RRSP, RIF, TFSA, RESP, RDSP, non-reg) and insurance with corporate strategies for maximum benefit to the family.

All services →How We've Helped Business Owners

Illustrative examples with real math. Every situation is unique, but the patterns are consistent.

The Compounding Tax Bomb

A growing business faces a $53-61M tax bill at death. Purification and estate freeze save ~$7M.

Read case study →Paying Pennies on Estate Tax

After an estate freeze, a $300K tax bill. Corporate life insurance funds it for 40-60% less than retained earnings.

Read case study →Active Trading to Tax-Free Estate

A 49-year-old redirects $3M from corporate trading into a structure designed for tax-free family wealth.

Read case study →All case studies are illustrative. Results vary by individual circumstances.

Resources & Learning

Start Here

If you have corporate surplus and aren't sure what to do with it, start with these:

- Your Corporation Made Good Money. Now What?

- The Boxes: How CRA Reaches Your Corporate Cash

- HoldCo/OpCo Structure Explained

See the Math

Case studies with real numbers showing how structure, insurance, and timing affect outcomes:

- The Compounding Tax Bomb

- From Active Trading to Tax-Free Estate

- Private Lending vs Corporate Investing

A Message from Your Advisor

Anton Ivanov

"Your corporation is your life's work. My job is to give you the discipline and tax-smart framework to protect and grow that wealth for generations. We're not investing for the next quarter; we're building wealth that lasts."

"As an independent advisor for incorporated professionals and their families, I've spent my career on the challenges you face: passive income rules, structure, estate strategy. Let's build a framework that endures."

How We WorkFrequently Asked Questions

Is corporate investing the same as personal?

No. Corporate accounts face different tax treatment. Prioritizing efficient income types and deferral often matters more than chasing headline yields.

Do you work only with one bank or insurer?

No. We're independent. We compare across providers and recommend what best fits your objectives and constraints.

Can you coordinate with my accountant and lawyer?

Yes. We regularly collaborate to align HoldCo/OpCo, trusts, estate freezes, and insurance design with your tax and legal plan.

Is this investment advice?

This website is educational. Advice requires a formal engagement, KYC/KYP, and suitability assessment based on your circumstances.